Since the end of the second quarter, the SP500 has experienced increased volatility and managed to bounce around between two major levels: the 200-day moving average which is traditionally acting as a support level and the all-time highs at the 3000 mark, acting as resistance.

There are multiple reasons for the churning action, from geopolitical uncertainty to elevated valuation multiples for many sectors. Markets are pulled in many conflicting directions and as discussed in previous blogs, they have cornered the Federal Reserve into preventive action and more monetary easing. As financial frictions rise, absent fiscal policy moves, the Fed will feel the urgency to step in and “grease” the economic wheels. One worry is the rising probability of a recession. Bloomberg Economics’ model estimates the chances of a recession in the next twelve months at 27%. This level is higher than a year ago but much lower than before the last economic contraction.

In fact, the labor market is still a bright spot in the macro-economic landscape as the unemployment level continues to stay at historically low percentages while real wages are growing at a slow but positive pace. As of now, markets are still operating under the assumption of a mid-cycle slowdown that central bankers and hopefully a more conciliatory trade policy can turn around.

From an investor’s perspective, one must also remember that not all recession are alike and therefore market reactions can also be very different. Not every recession will have the same devastating effects of the 2008 debacle. Actively trading around recessionary perceptions is a very difficult endeavor and usually tends to become a value destruction exercise. A recent study by Putnam, shows that by missing out the best ten days of the market in the last 15 years, an investor would have seen his/her account cut in half. Missing out the twenty best days would have reduced the account by approximately 66%.

As discussed in previous missives, the best way to prepare for significant volatility is to get the process of asset allocation right at the start by including many variables and not just the probability of a possible recession.

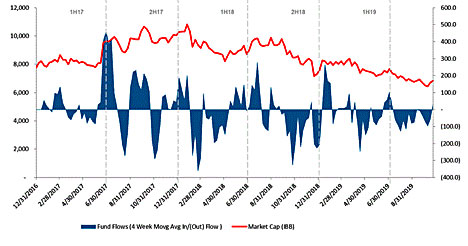

Sector Focus: Biotech

The Biotech sector has been on a road to nowhere for quite some time. When measured by the larger biotech names (IBB), performance has been practically stale for 4 years, as the sector has been digesting the great run from the 2009 lows. The situation is somewhat better in the small cap part of the field (XBI) where performance has been stuck for about 2 years. Valuations and uncertainty on the political front in regards to product prices and reimbursements have made investors cautious. However, the long churning has made many names very attractive while the future pipeline of products is shaping up to be one of exciting new cures. The convergence of big data with empirical research, the steps taken in gene therapy and the generally unforeseen developments in oncology are lighting excitement under the sector.

As the chart below implies, in the last two weeks we are beginning to see a reversal of fund flows (from negative to positive) which also coincided with outperformance of the SP500 benchmark index (2.5% vs. 0.4% for the SP500). Feel free to contact our team, should you want to discuss the sector in more details.