There are multiple reasons why an investor should be looking at the biopharma sector with interest and intrigue. For one, the mission of this modern science is of the greatest order: to help people live better and longer lives. Strategically, such mission is nowadays helped by an accelerating innovation process which is benefitting from different dynamics such as the increasingly intertwined relationship between traditional pharmaceutical research and the rise of Big Data.

The new disruptive wave is generating evolving trends. A most important one is concerned in targeting medical issues in a significantly more precise way. Customized treatments result in less side effects and possibly in a more efficient allocation of resources within our health care system.

Research disruption has also helped the industry reshape the product pipeline which had been suffering by some disappointments, longer than expected lead times and probably too many “me-too” drugs.

Venture capitalist Davide Epstein, a partner at VC firm Flagship Pioneer, also points out the improved financial landscape where companies with issues in funding all of their pipeline projects have been able to structure different alternative ventures or manage spinouts in order to implement a more comprehensive portfolio of projects.

To put biopharma potential in the proper context, a McKinsey paper from December 2014 quotes revenues directly linked to the subsector at $163 billion which represent 20% of the overall pharma market. Biopharma is the fastest growing part of the industry at an 8% annualized growth rate, twice as fast as the rate of traditional pharma.

The acceleration of biotech is also visible in the number of patents applied yearly which has been growing at 25% annually since 1995. No area of research is left untouched as interesting innovations are emerging in immunotherapy, gene and cell therapy.

Another interesting reason to look at this sector, is that attractive long term growth prospects are currently priced in a reasonable fashion as opposed to a general market which is increasingly expensive.

While the sector has enjoyed a good recovery since the Presidential Election lows, it is still far from its previous high recorded in 2015.

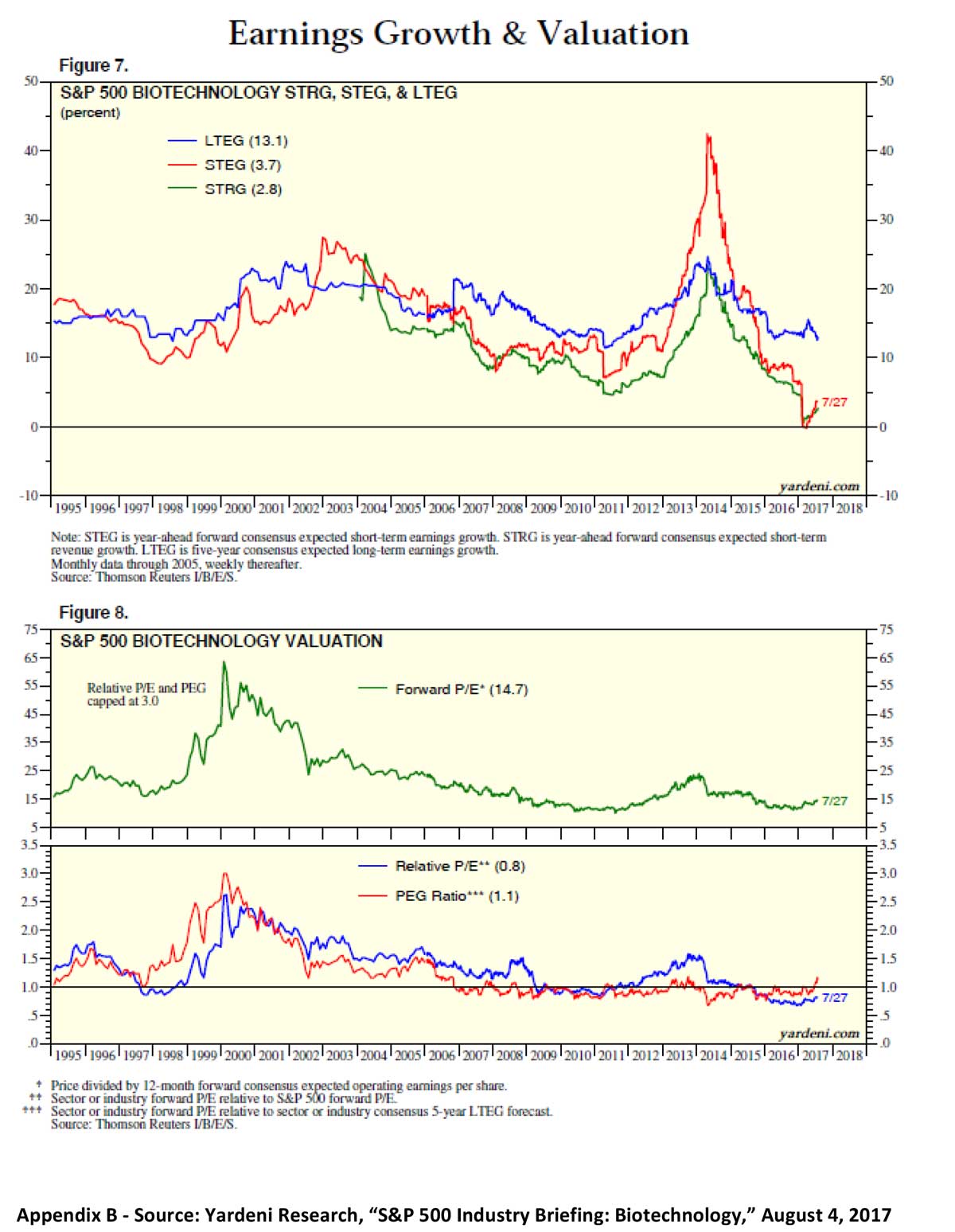

Appendix B and Appendix C, at the end of this piece, provide a few valuation metrics on the sector within an historical framework.

The Morningstar Fair Value model (based on a proprietary discounted cash-flow model) shows the Biotech sector 6% undervalued. Furthermore, Yardeni Research shows how the Forward P/E ratio of the sector and the Relative P/E ratio (relative to the Price/Earnings ratio of the S&P 500) are around historical lows.

Part of the valuation discount can be attributed to the political uncertainty surrounding the health care industry in general. Frequent attacks from both sides of the aisle on the pricing of medicines and treatments and the inability of Congress to enact articulated legislation on health care has certainly kept away many investors. This is indeed a hard element to forecast as the whole political process has been characterized by a significant amount of confusion and illogical decision making. However, the disruptive nature of the sector and the potential benefits, both in terms of human improvements and economic opportunity, would seem to provide a strong incentive for politicians and administrators alike to avoid taking decisions that could be seriously negative for Biopharma.

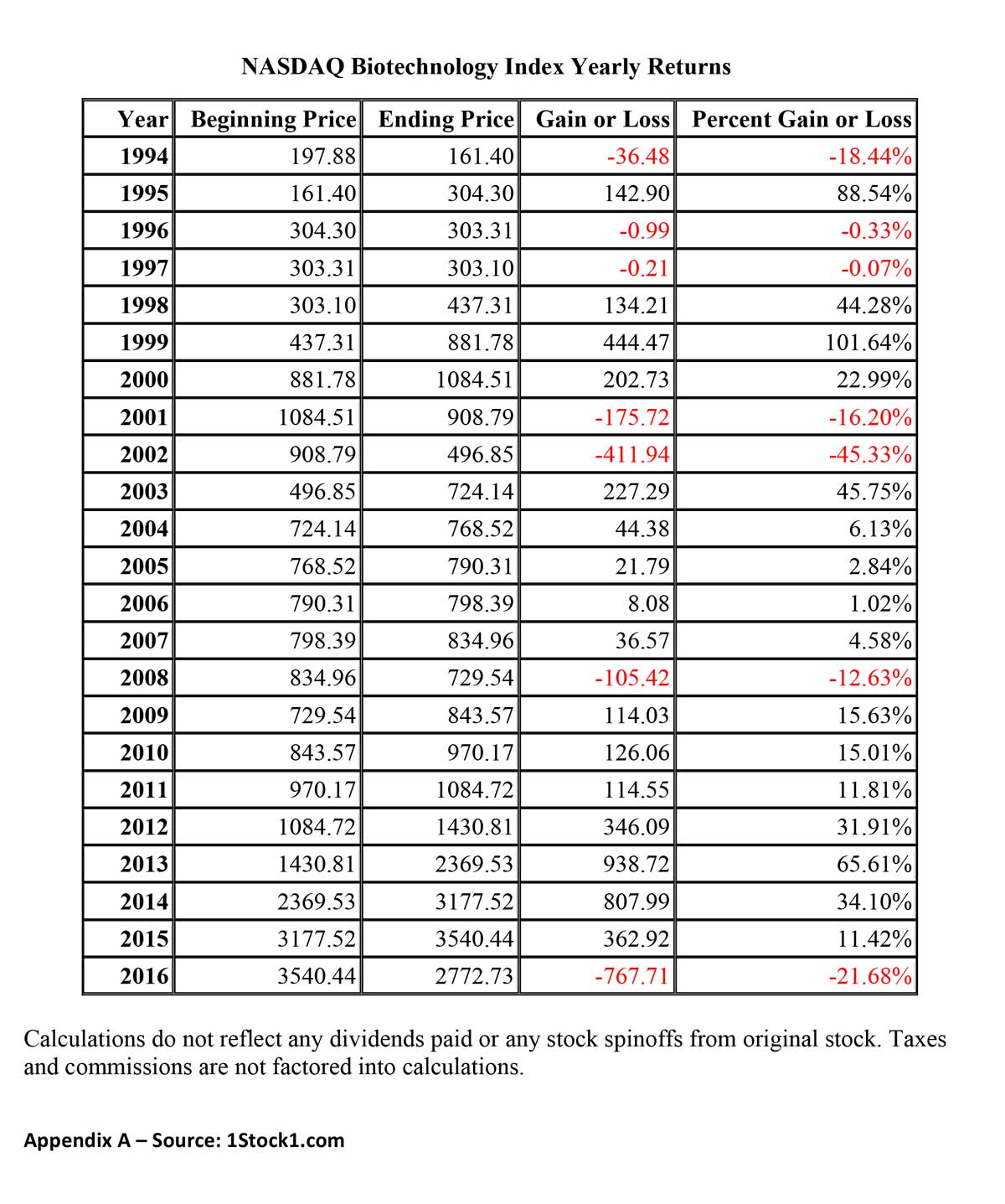

In order to help with the historical context, Appendix A provides yearly returns for the Nasdaq Biotech Index from 1994 to 2016. Naturally, this is only an indication of risk and opportunities in the sector as investors’ actual return will always be a function of their actual security selection and market timing.

At THALASSA CAPITAL, we have created a new portfolio geared toward the biotech sector where we have attempted to combine the higher rate of opportunities available in the small cap part of the investable universe along with exposure to the large cap segment of the more traditional pharma.

Please call our team should you desire to discuss further.